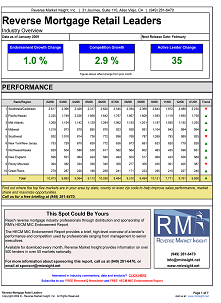

HECM endorsements for November rose 12% to 4,690 loans, marking the impact of standard ARM applications taken before the Sep 30th program changes. We expect to see endorsements continue to be relatively strong for the next few months, but turn significantly lower toward the end of Q1 next year. New applications are falling well short of replacing pipeline fundings since principal limits were reduced.

On the bright side, despite all the program changes this year it’s been a growth period for the industry with volume up 15.9% through November, including 9 straight months of year over year increases since March. That coincides fairly closely with housing price upticks over the same time frame, but it’s more a case of no significant lender exits upsetting distribution and marketing reach this year alongside stabilized housing prices (which have been conducive to HECM growth since at least 2011).

Among the regions, 7 of 10 were up in November including a big 206 loan increase (23.6%) in Pacific/Hawaii and 32.3% increase in Mid-Atlantic. Phoenix continues to power a remarkable comeback, up 64.7% over last Jan-Nov and not a single metro is down in the region.

Among lenders, 6 of 10 were up, with another flat for the month.

Click the image below for the full report.